1. What are stock options?

A stock option is a standardised contract with a stock as the underlying asset, thus it can be traded on an exchange and settled by a clearing house.

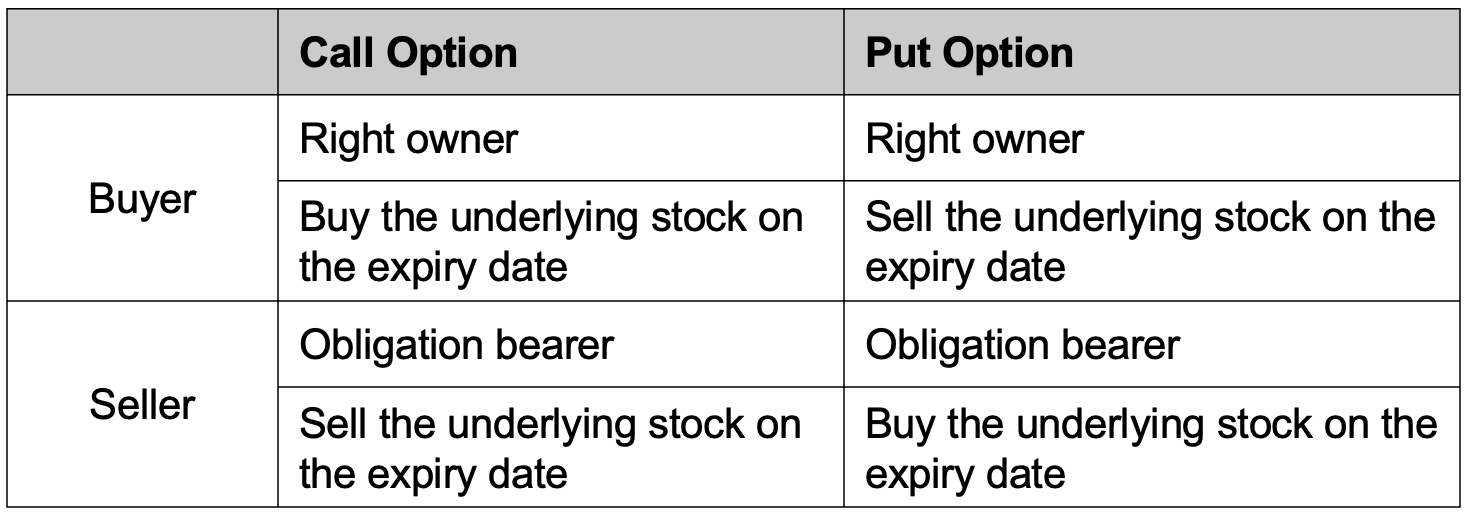

- Stock options can be divided into call options and put options according to the differences of rights between right owners;

- American options and European options according to the exercise method;

- Cash settlement and physical delivery according to the settlement method. Most U.S. stocks and HK stocks are American options based on physical delivery, while index options are generally European options based on cash settlement.

In terms of stock options, the buyer is the right owner while the seller is the obligation bearer.

- The buyer of an American call option has the right to buy the underlying stock at the strike price on or before the expiry date of the contract, and the seller of the call option is obliged to sell the underlying stock at the strike price if the option is exercised.

- The buyer of an American put option has the right to sell the underlying stock at the strike price on or before the expiry date of the contract, and the seller of the put option is obliged to buy the underlying stock at the strike price if the option is exercised.

European option can only be exercised on the contract's expiry date.

2. What is Option Premium?

An option premium is the trading price of an option and the only variable in a standardised contract.

For options traded on an exchange, the price is displayed on a per-share basis, and the minimum trading contract is 1. Generally, 1 contract for U.S. stock options represent 100 shares. The buyer (right's owner) pays the option premium to receive the right and the seller (obligation's bearer) charges option premium to fulfill the obligation.

Option premium= Option price x Contract size x Option multiplier

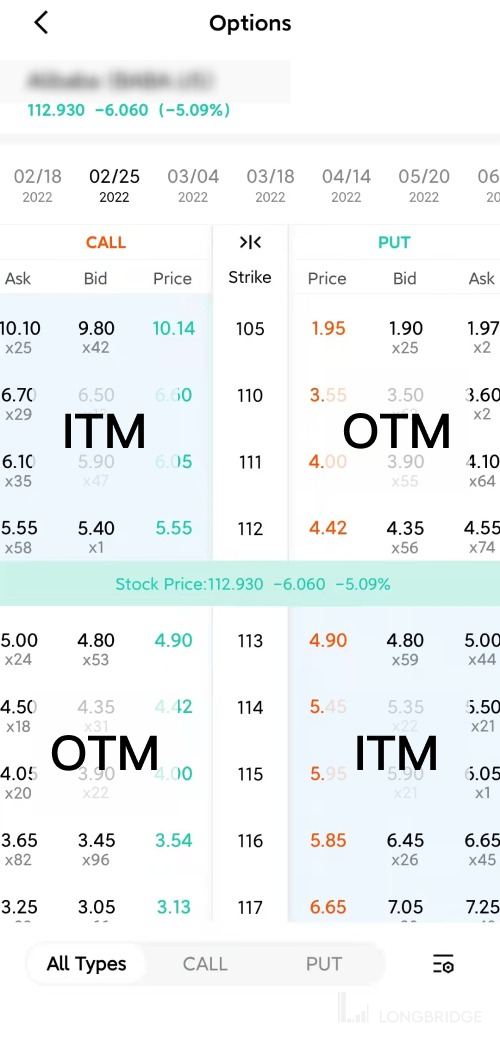

3. What is OTM/ITM?

- OTM - Out the Money

- ITM - In the Money

Every option has a strike price, so options can be divided into OTM & ITM according to the agreed strike price and the stock’s market price fluctuations. The difference between OTM and ITM is whether the option has real value at the moment.

How to determine if the call option is ITM/OTM:

When the stock price > the strike price = ITM; otherwise, it is OTM

How to determine if the put option is ITM/OTM:

When the strike price > stock price = ITM; otherwise, it is OTM

An option is an ITM when it has real value.

When trading with Longbridge, you can find that ITM/OTM options have distinct colors on the options chain page, and the blue part under the T-style layout is ITM options.

4. Four Basic P&L Calculations for Options Trading

Long call options

It gives the right to buy the underlying stock at the agreed price when it expires.

P&L Calculation

For example:

Suppose a trader buys (Long) a call option (Call) at the option premium of USD 5, with a total payout of USD 500.

Two elements:Strike Price = 50

Contract Size = 100

The following situations will occur:

- The stock market price is USD 40, and the stock market price < strike price USD 50. When the trader exercises the option, the P/L of each call option purchased = (40-50-5) * 100 = USD -1500. The maximum loss for waiving the exercise rights is the paid option premium of USD 500, which is lower than the loss for exercising the option. Therefore, most traders choose not to exercise.

- The stock market price is USD 50, and the stock market price = strike price USD 50. When the trader exercises the option, the P/L of each call option purchased = (50-50-5) * 100 = USD -500. The maximum loss for waiving the exercise rights is the cost of the paid option premium of USD 500, which equals the option premium. Therefore, most traders choose not to exercise.

- The stock market price is USD 60, and the stock market price = strike price USD 60. When the trader exercises the option, the P/L of each call option purchased = (60-50-5) * 100 = USD 500. The loss for waiving the exercise rights is the paid option premium of USD 500. Most traders choose to sell during the session, while a few choose to exercise the option to acquire the stock and sell the stock after delivery.

Long put options

It gives the right to sell the underlying stock at the agreed price when it expires.

P&L Calculation

For example:

Suppose a trader buys (Long) a put option (Put) at the option premium of USD 5, with a total payout of USD 500

Two elements:

Strike Price = 50

Contract Size = 100

The following situations will occur:

- The stock market price is USD 40, and the stock market price < strike price USD 50. When the trader exercises the option, the P/L of each put option purchased = (50-40-5) * 100 = USD 500. The trader will not gain the return if waiving the exercise rights and loss will be the paid option premium of USD 500. Most traders choose to sell during the session, while a few choose to exercise the option and sell the stock.

- The stock market price is USD 50, and the stock market price = strike price USD 50. When the trader exercises the option, the P/L of each put option purchased = (50-50-5) * 100 = USD -500. The maximum loss for waiving the exercise rights is the cost of the paid option premium of USD 500, which equals the option premium. Therefore, most traders choose not to exercise.

- The stock market price is USD 60, and the stock market price = strike price USD 60. When the trader exercises the option, the P/L of each put option purchased = (50-60-5) * 100 = USD -1500. The loss for waiving the exercise rights is the paid option premium of USD 500, which is lower than the loss for exercising the option. Therefore, most traders choose not to exercise.

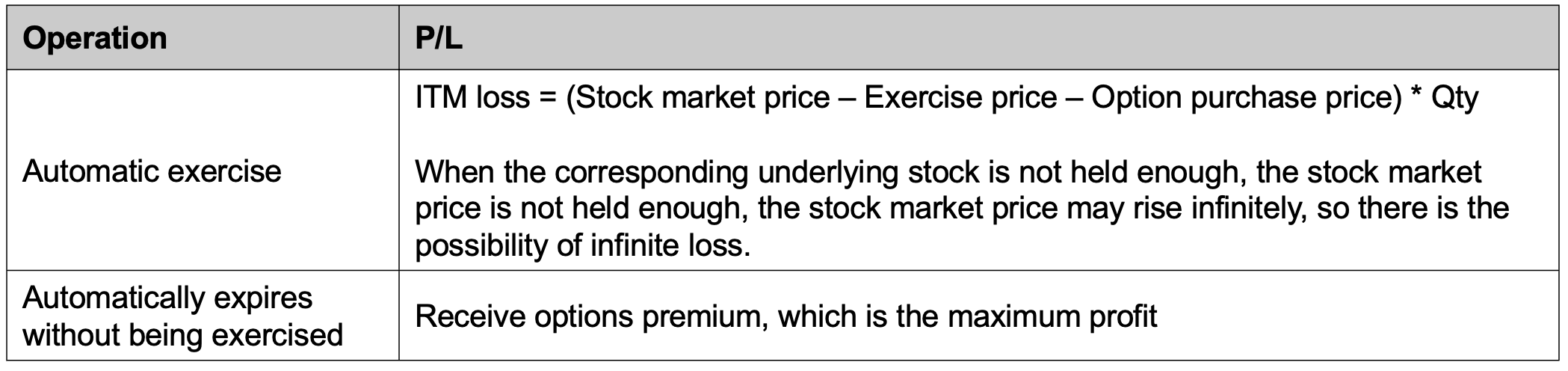

Short call options

It stipulates the obligation to sell the underlying stock at the agreed price when it expires.

P&L Calculation

For example:

Suppose a trader sells (Short) a call option (Call) at the option premium of USD 5, and gets the option premium of USD 500.

Two elements:

Strike Price = 50

Contract Size = 100

The following situations will occur:

- The stock market price is USD 40, and the stock market price < strike price USD 50.

P/L of selling call options at the expiry date when being automatic exercised = [-max (40-50,0)+ 5)]*100. The trader is assigned a gain of USD 500 in the options contract on the exercise. In the OTM situations, there are very few cases where automatic exercise is assigned.- The stock market price is USD 50, and the stock market price = strike price USD 50.

P/L of selling call options at the expiry date when being automatic exercised = [-max (50-50,0)+ 5)]*100. The trader is assigned a gain of USD 500 in the options contract on the exercise.- The stock market price is USD 60, and the stock market price = strike price USD 60.

P/L of selling call options at the expiry date when being automatic exercised = [-max (60-50,0)+ 5)]*100. The trader is assigned a loss of USD 500 in the options contract on the exercise.

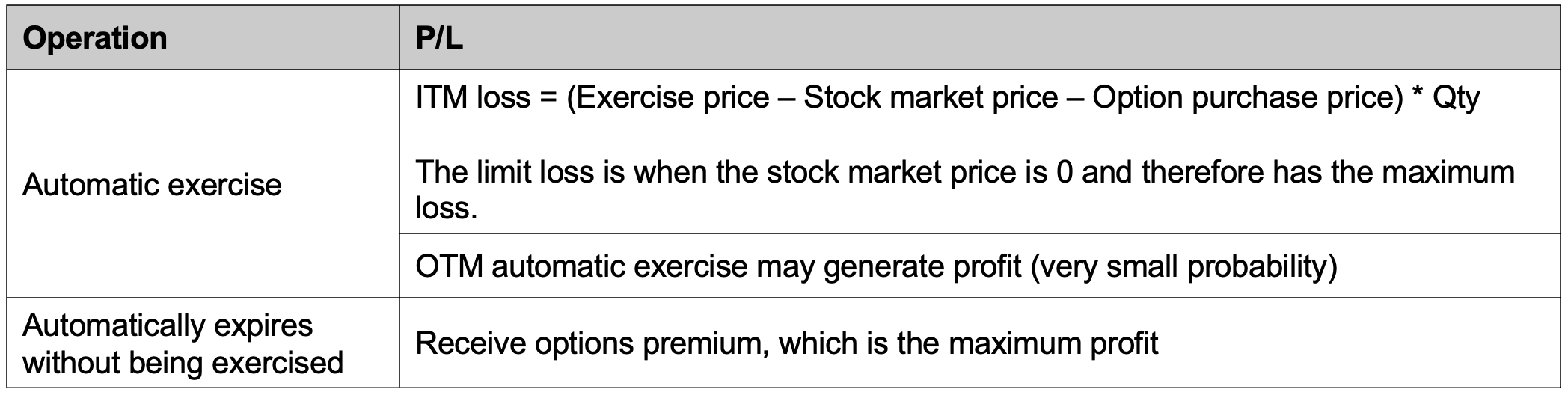

Short put options

It stipulates the obligation to buy the underlying stock at the agreed price when it expires.

P&L Calculation

For example:

Suppose a trader sells (Short) a put option (Put) at the option premium of USD 5, and gets the option premium of USD 500.

Two elements:

Strike Price = 50

Contract Size = 100

The following situations will occur:

- The stock market price is USD 40, and the stock market price < strike price USD 50.

P/L of selling put options at the expiry date when being automatic exercised = [-max (50-40,0) + 5) ]*100. After the trader is assigned to automatic exercise, they obtain 100 shares of the underlying stock at the exercise price of USD 50. If the market price remains unchanged, the obtained stock will lose USD 1000, and the option will earn USD 500. The balance is USD -500.- The stock market price is USD 50, and the stock market price = strike price USD 50.

P/L of selling put options at the expiry date when being automatic exercised = [-max (50-50,0) + 5) ]*100. After the trader is assigned to automatic exercise, they obtain 100 shares of the underlying stock at the exercise price of USD 50. If the market price remains unchanged, they can earn the options return of USD 500.- The stock market price is USD 60, and the stock market price = strike price USD 60.

P/L of selling put options at the expiry date when being automatic exercised = [-max (50-60,0) + 5) ]*100. After the trader is assigned to automatic exercise, they obtain 100 shares of the underlying stock at the exercise price of USD 50. If the market price remains unchanged, they can earn the options return of USD 500. Rarely will the buyer exercise the option in this situation.

5. Exercise & Settlement

Exercise Instructions

If a user still holds an options position after the option expires, Longbridge will “exercise the option” or “waive the exercise rights” on the user’s behalf. At present, Long Bridge does not support the manual exercise of options.

Exercise:

- ITM options are exercised before the market opens on the next trading day.

- Call options: If strike price < underlying stocks’ settlement price, then they are ITM options.

- Put options: If strike price > underlying stocks’ settlement price, then they are ITM options.

After exercising the option:

- Call options: The user will buy the corresponding underlying stock at the exercise price. After the exercise of the option, the funds for buying the underlying stock will be deducted, and the underlying stock obtained by the exercise will be added to the user’s position.

- Put options: The user will sell the corresponding underlying stock at the exercise price. After the exercise of the option, the underlying stock will be deducted, and the user will get the funds for selling the underlying stock.

Waive

- OTM options will be waived before the market opens on the next trading day.

- Call options: If strike price > underlying stocks’ settlement price, then they are OTM options.

- Put options: If strike price < underlying stocks’ settlement price, then they are OTM options.

After waiving the exercise rights

- The user’s position will be null and void for either call options or put options.

Settlement

Both options and underlying stocks are settled on T+1.

Options Trading FAQs

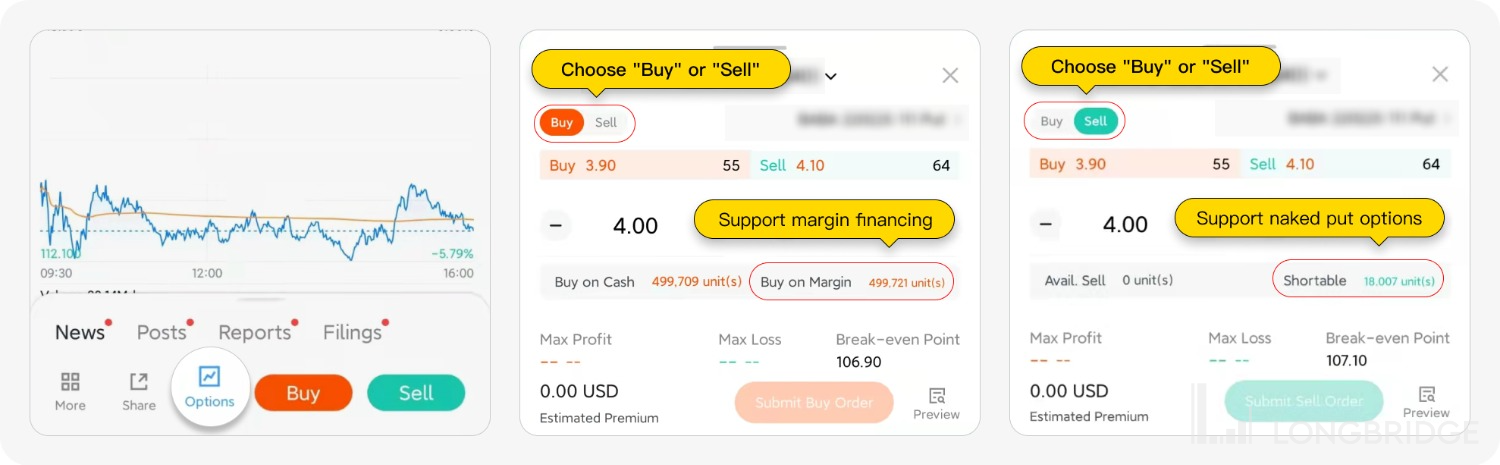

Q1: How to trade options?

Enter the options chain page in the stock details page, tap the corresponding option, activate the quick trade drawer, select buy or sell, enter the corresponding price and quantity to place an order.

Q2: What are the supported order types for options?

Currently, options trading supports limit orders, market orders, conditional orders and long-term orders.

Q3: What is the minimum trading unit for options?

An option is a standardised contract with a minimum trading volume of 1 unit. Generally, 1 contract unit equals 100 shares (corporate actions may result in 1 option not being equal to 100 shares).

For example, in the case of options contract SPY 220304 C 429000, its options premium is USD 6.68. Therefore, a total of $ 6.68 * 100 = $ 668 needs to be paid for holding this option. Upon exercise, 100 shares of SPY will be received.

Q4: What are the trading hours for options?

The trading hours for U.S. stock options are 9:30~16:00 EST

Daylight saving time (March - November). The above time corresponds to 21:30 - 04:00 (GMT+8)

Standard time (November - next March). The above time corresponds to 22:30-05:00 (GMT+8)

Note: Most U.S. stock options do not support pre&post-market trading, but some ETF and ETN options can be extended until 16:15 EST.

Q5:Why Is the Margin Requirement Higher for Close-to-Expiry Options?

For options expiring within the same trading day (i.e., same-day expiry options), an additional margin requirement is imposed at 10:00 AM EST. This is to ensure that clients maintain sufficient funds to support potential exercise obligations should the option expire in-the-money (ITM) — particularly when the underlying price moves within ±2% of the strike price. It is important to note that the same procedure also applies to options purchased on their expiry date.

If a client lacks sufficient funds or the necessary underlying stocks to cover the potential exercise, their account may be flagged as "dangerous" and trigger a margin call. If the margin call is not resolved, an automatic force-selling will be executed.

To avoid forced liquidation, clients should address margin calls by liquidating their options position or by successfully depositing additional funds.

Corporate Actions & Special Situations

In the case of corporate actions and other special situations, the user's current positions will be transferred to a new position, where the option value will not change, but the underlying stock corresponding to the option may change.

For example, 1 unit of BABA option corresponds to 100 shares of BABA underlying stock. If BABA issues a reverse stock split, 1 new share for 5 old shares, then the equity of each option equals 20 shares of BABA after consolidation, and the entire equity value does not change.

New positions, as a result of corporate actions, can be closed but not opened.

Disclosures

This article is for reference only and does not constitute any investment advice.

- Contact Us

- WhatsApp Chat (for general enquiries):+65 6330 3035

- Trading days: 9:00am – 6:00pm (GMT+8)

- Dealing Hotline:+65 6330 3030

- Trading days: 9:00am – 6:00pm (GMT+8)

- For Institutions

- Corporate Services

- OpenAPI

- contact@longbridge.sg

- About

- About us

Registered with the Monetary Authority of Singapore (MAS), Long Bridge Securities Pte. Ltd. is a Capital Markets Services Licence holder and Exempt Financial Adviser (Licence No. CMS101211).

A licensed corporation recognized by the SFC (CE No. BPX066). Holder of License Types 1 (Dealing in Securities), 2 (Dealing in Futures Contracts), 4 (Advising on Securities) and 9 (Asset Management). Also a registered HKEX participant and HKSCC participant.

Long Bridge Securities LLC

Long Bridge Securities LLCA broker dealer registered with the Securities and Exchange Commission (SEC)(CRD: 314519/SEC: 8-70711), a member of the Financial Industry Regulatory Authority (FINRA) and Securities Investor Protection Corporation (SIPC).

A New Zealand registered Financial Service Provider (FSP number: FSP600050), and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

Long Bridge Securities Pte. Ltd. (“Long Bridge Securities”) (UEN No.: 202111825D) is regulated by the Monetary Authority of Singapore and holds a Capital Markets Services Licence for dealing in capital markets products that are securities, collective investment schemes, and exchange-traded derivatives contracts, and is an Exempt Financial Adviser.

The information contained on this website is provided for general information and educational purposes only. It does not take into account your specific investment objectives, financial situation, or particular needs. The content on this website does not constitute financial advice, an investment recommendation, an offer, or a solicitation to buy or sell any financial product.

You should carefully consider the suitability of any investment in light of your own circumstances, including your investment objectives, financial situation, and risk tolerance. Where necessary, you should seek advice from an independent financial adviser under a separate engagement before making any investment decision.

All investments carry risks. The value of financial instruments and products may rise or fall, and you may lose all or more than your initial investment. Past performance is not necessarily indicative of future results. Certain products, such as margin trading, options, warrants, exchange-traded derivatives, and structured products, involve a high degree of risk and may not be suitable for you.

Before trading, you must read the relevant risk disclosure statements available on the Longbridge Risk Disclosure Statement page.

While Long Bridge Securities takes reasonable care to ensure that the information provided on this website is accurate as at the time of publication, no representation or warranty is made as to its accuracy, adequacy, completeness, or reliability. Information may be subject to change without notice. Long Bridge Securities shall not be liable for any loss or damage arising from any reliance on or use of the information contained on this website.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

In the event of any discrepancy or inconsistency between the English version and the Chinese translation, the English version shall prevail.