This article details the call mechanism of Hong Kong Callable Bull/Bear Contracts (CBBCs), using examples to explain the settlement methods for bull and bear contracts (Category R) under different scenarios, as well as how residual value is settled after a CBBC expires or is called.

1. Call mechanism of CBBCs

From the listing date until the trading day before expiry, if the price of the underlying asset touches the call price on any day, the mandatory call mechanism is triggered, and the trading of that CBBC ceases immediately.

When the call price is triggered:

Category R | Strike price ≠ Call price. The settlement price of the CBBC is calculated based on the lowest price (for bull certificates) or highest price (for bear certificates) of the underlying asset from the time of mandatory call to the end of the next trading session. If the lowest price (bull) or the highest price (bear) is at or exceeds the strike price, the CBBC may have no residual value. |

|---|

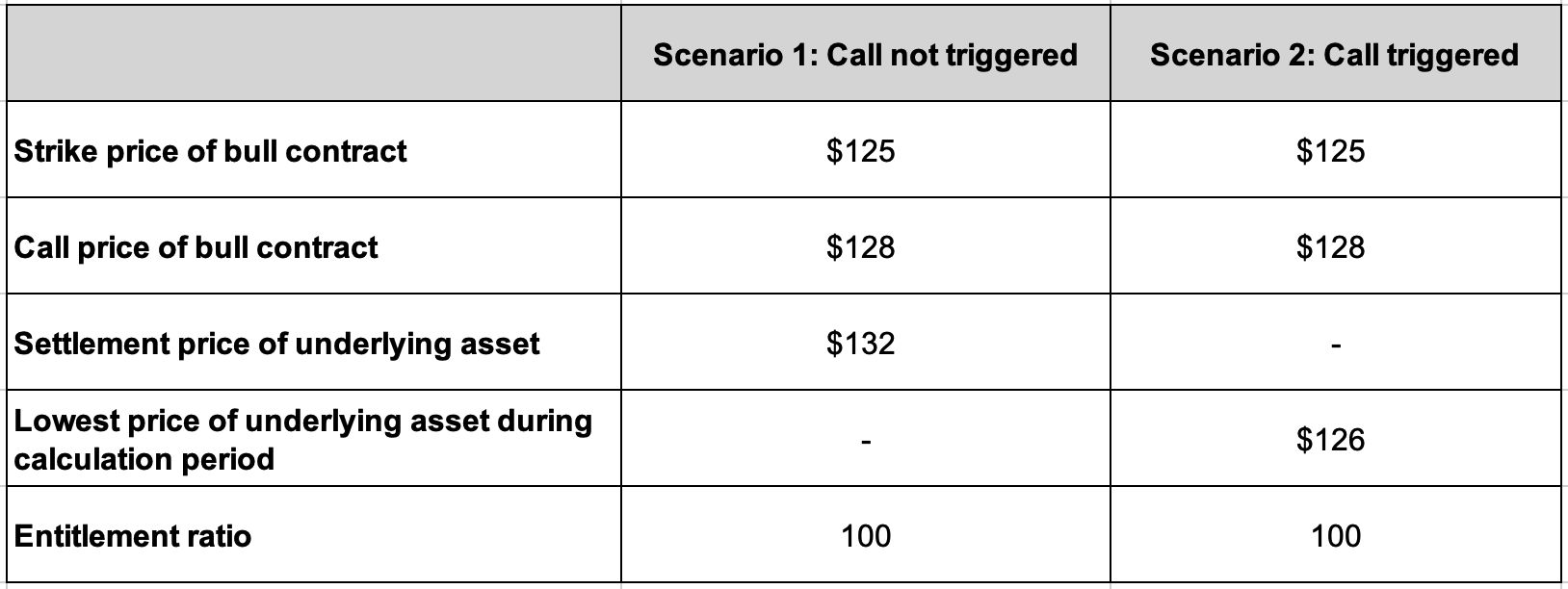

2. Settlement method for bull certificates (example)

Example

Scenario 1: call price not triggered

Amount you can receive:

= (Underlying security settlement price – Bull certificate strike price)/Conversion ratio

= (USD 132–USD 125)/100

= USD 0.07all price not triggered

Scenario 2: call price triggered

Amount you can receive:

= (Lowest price of the underlying security – Bull certificate strike price)/Conversion ratio

= (USD 126–USD 125)/100

= USD 0.01

Generally, the settlement price for CBBCs is the closing price of the underlying stock on the last trading day before expiration. For index-based CBBCs, the settlement level is the futures settlement level of the expiration month. You can refer to the listing documents for specific details on settlement prices.

The lowest price is the spot lowest price from the time of mandatory call until the end of the next trading session. If called in the morning, valuation continues until the afternoon session; if called in the afternoon, valuation continues until the noon session of the next trading day. In the worst case, if the lowest price is at or below the bull certificate strike price, you may receive no residual value.

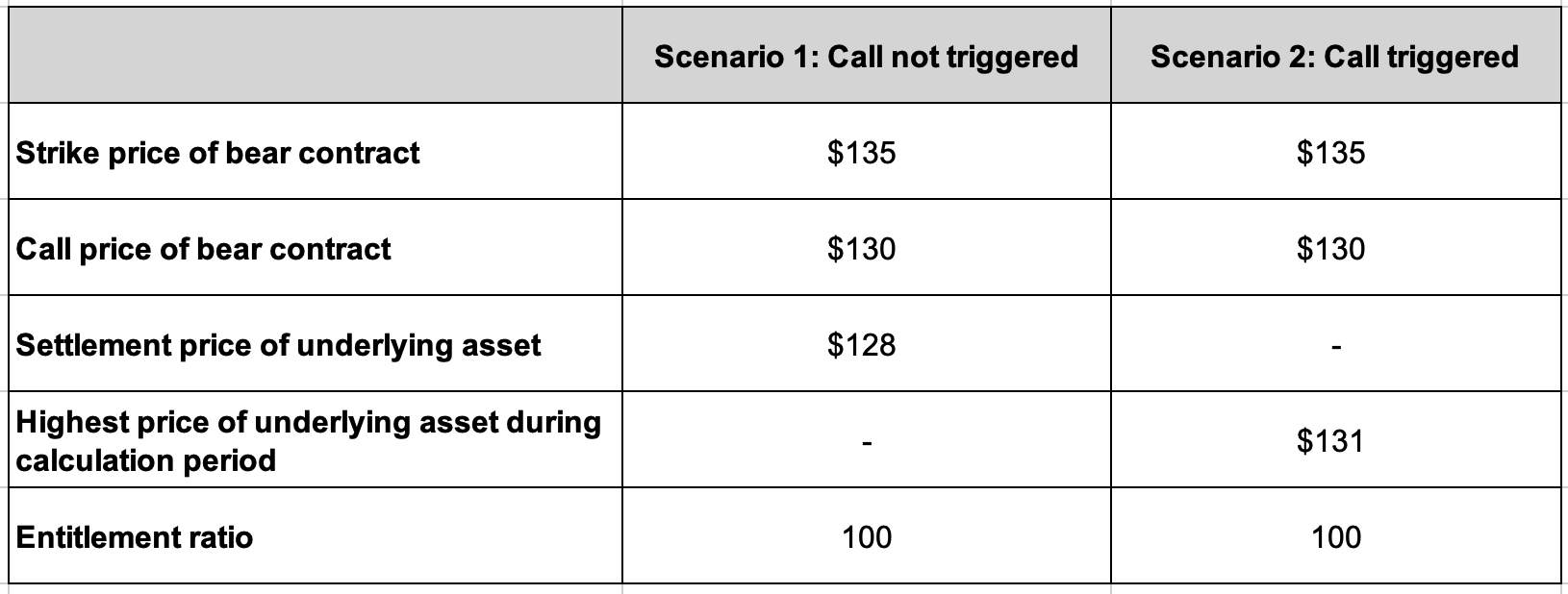

3. Settlement method for bear certificates (Category R) (example)

Scenario 1: call price not triggered

Amount you can receive:

= (Bear certificate strike price – Underlying security settlement price)/Conversion ratio

= (USD 135–USD 128)/100

= USD 0.07

Scenario 2: call price triggeredAmount you can receive:

= (Bear certificate strike price – Highest price of underlying security)/Conversion ratio

= (USD 135–USD 131)/100

= USD 0.04

Generally, the settlement price for CBBCs is the closing price of the underlying stock on the last trading day before expiration. For index-based CBBCs, the settlement level is the futures settlement level of the expiration month. You can refer to the listing documents for specific details on settlement prices.

The highest price is the spot highest price from the time of mandatory call until the end of the next trading session. If called in the morning, valuation continues until the afternoon session; if called in the afternoon, valuation continues until the noon session of the next trading day. In the worst case, if the highest price is at or above the bear certificate strike price, you may receive no residual value.

4. Settlement of residual value after CBBC expiration or call

No additional action is required from you after a CBBC expires or is called. It is recommended to check the daily statement for details.

If there is residual value, it will be automatically deposited into your account by Longbridge within one week after the issuer completes the settlement. The corresponding CBBC is expected to disappear from the holdings within one week. Please refer to the issuer's announcement for details. You may check the residual value of warrants/CBBCs via the following link: https://warrants.ubs.com/en/cbbc/residual-value-of-cbbc.

Disclosures

This article is for reference only and does not constitute any investment advice.

- Contact Us

- WhatsApp Chat (for general enquiries):+65 6330 3035

- Trading days: 9:00am – 6:00pm (GMT+8)

- Dealing Hotline:+65 6330 3030

- Trading days: 9:00am – 6:00pm (GMT+8)

- For Institutions

- Corporate Services

- OpenAPI

- contact@longbridge.sg

- About

- About us

Registered with the Monetary Authority of Singapore (MAS), Long Bridge Securities Pte. Ltd. is a Capital Markets Services Licence holder and Exempt Financial Adviser (Licence No. CMS101211).

A licensed corporation recognized by the SFC (CE No. BPX066). Holder of License Types 1 (Dealing in Securities), 2 (Dealing in Futures Contracts), 4 (Advising on Securities) and 9 (Asset Management). Also a registered HKEX participant and HKSCC participant.

Long Bridge Securities LLC

Long Bridge Securities LLCA broker dealer registered with the Securities and Exchange Commission (SEC)(CRD: 314519/SEC: 8-70711), a member of the Financial Industry Regulatory Authority (FINRA) and Securities Investor Protection Corporation (SIPC).

A New Zealand registered Financial Service Provider (FSP number: FSP600050), and is a member of the Financial Dispute Resolution Scheme, a New Zealand independent dispute resolution service provider.

Long Bridge Securities Pte. Ltd. (“Long Bridge Securities”) (UEN No.: 202111825D) is regulated by the Monetary Authority of Singapore and holds a Capital Markets Services Licence for dealing in capital markets products that are securities, collective investment schemes, and exchange-traded derivatives contracts, and is an Exempt Financial Adviser.

The information contained on this website is provided for general information and educational purposes only. It does not take into account your specific investment objectives, financial situation, or particular needs. The content on this website does not constitute financial advice, an investment recommendation, an offer, or a solicitation to buy or sell any financial product.

You should carefully consider the suitability of any investment in light of your own circumstances, including your investment objectives, financial situation, and risk tolerance. Where necessary, you should seek advice from an independent financial adviser under a separate engagement before making any investment decision.

All investments carry risks. The value of financial instruments and products may rise or fall, and you may lose all or more than your initial investment. Past performance is not necessarily indicative of future results. Certain products, such as margin trading, options, warrants, exchange-traded derivatives, and structured products, involve a high degree of risk and may not be suitable for you.

Before trading, you must read the relevant risk disclosure statements available on the Longbridge Risk Disclosure Statement page.

While Long Bridge Securities takes reasonable care to ensure that the information provided on this website is accurate as at the time of publication, no representation or warranty is made as to its accuracy, adequacy, completeness, or reliability. Information may be subject to change without notice. Long Bridge Securities shall not be liable for any loss or damage arising from any reliance on or use of the information contained on this website.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

In the event of any discrepancy or inconsistency between the English version and the Chinese translation, the English version shall prevail.